Read a most interesting analysis on social media predicting that Anthropic will surpass Google in revenue by 2028.

On the surface, this prediction seems fanciful.

But, given Anthropic’s unprecedented growth in ARR this year alone, it’s worth considering.

Before we get to the prediction, just listen to David Sacks putting into perspective Anthropic’s historic ARR growth. Even he suggests it might hit $1 trillion in 2027.

Here’s the prediction of Anthropic surpassing Google:

I asked Claude to assess this prediction. Claude had some criticisms, none of which strike me as preclusive:

- Specific timing overconfidence: Treating mid-2028 as mechanical rather than probabilistic understates the enormous variance around any unprecedented growth trajectory.

- “Deceleration” framing is misleading: Calling a path from $30B to $850B in 27 months a deceleration uses the word in a technical sense that obscures how aggressive the absolute trajectory remains.

- Labor TAM ≠ addressable revenue: The $50T figure is a ceiling on economic activity, not a pool Anthropic can extract from, since wages don’t convert cleanly into AI provider revenue under competitive market dynamics.

- Single-firm capture assumption: The argument needs Anthropic specifically to dominate, but OpenAI, Google, Meta, xAI, Chinese labs, and open-weight alternatives all compete for the same workloads.

- Pricing power tension: The same compute supply release cited as bullish also enables competitors to scale, which historically compresses margins and pricing.

- Churn claim is asserted, not demonstrated: “Near-zero churn” relies on limited public data and ignores that multi-model architectures are increasingly standard specifically to prevent lock-in.

- Alphabet treated as static: Pinning Google at 15% YoY ignores its frontier model effort, distribution to billions of users, and deep TPU infrastructure that could reaccelerate growth.

- Weak signal in token comparison: Quarterly Gemini token growth reflects usage and pricing patterns, not competitive position or revenue, and one datapoint doesn’t establish a structural trend.

- Confidence should scale inversely with unprecedented-ness: The same category-shift argument that makes the upside plausible also widens the uncertainty band, which the prediction’s certainty doesn’t reflect.

Claude made its own predictions with various possiblities for Anthropic’s growth in revenues:

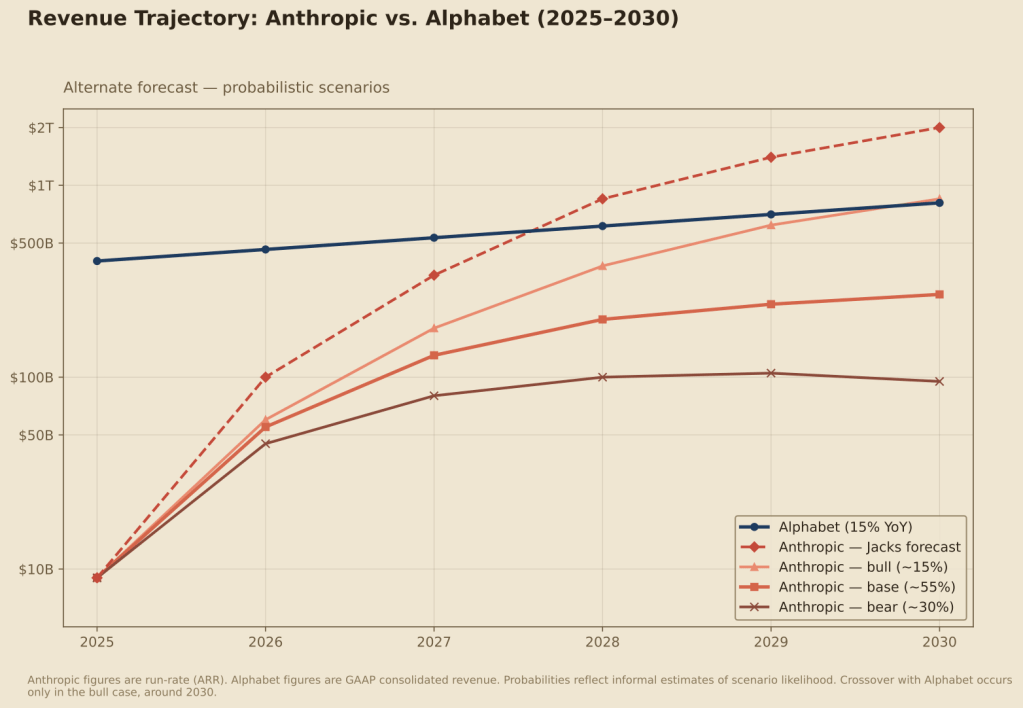

The original chart presents one deterministic line with a single crossover point in mid-2028. My alternate replaces that with a probability cone — three Anthropic scenarios with rough likelihoods attached, plotted on a log scale so the differences across orders of magnitude are visible.

The bull case (~15% probability) is the one that most resembles the original thesis spirit, but pushes the crossover to roughly 2030 rather than 2028. It assumes growth stays elevated longer than typical S-curves but still moderates as Anthropic moves past $200-300B — because even unprecedented businesses don’t sustain 3x annual growth indefinitely at hyperscale. This is where the labor-TAM thesis substantially holds.

The base case (~55% probability) is what I’d actually expect: extraordinary growth by any historical standard, reaching $250-300B by 2030, but with meaningful deceleration as competitive pressure, pricing compression, and the natural physics of large-number compounding kick in. No crossover with Alphabet in this window. This still has Anthropic becoming one of the largest companies in the world — just not the largest.

The bear case (~30% probability) accounts for scenarios the original prediction dismisses too quickly: a frontier-model commoditization wave, OpenAI or a Chinese lab pulling ahead on capability, enterprise budgets normalizing, or pricing pressure from open-weight alternatives compressing margins. Anthropic still ends up a major company, just one that plateaus closer to $100B.

The deeper methodological difference is that the original chart hides its uncertainty inside a confident-looking line. Mine surfaces it. The crossover question isn’t binary — it’s a probability distribution, and the honest forecast says there’s a real but minority chance of the original thesis being right, a larger chance of something dramatic but less extreme, and a non-trivial chance the trajectory disappoints relative to current expectations.

That we can even entertain this possibility without laughing out loud does signal how significant Anthropic’s current rate of ARR is.

We shall see what happens next.

Leave a comment